They can either sell a concentrate onwards to someone who would like to process it themselves or potentially modify the existing infrastructure (higher capex obviously) within the country to process it and sell the battery grade stuff. Or they could build a plant from scratch.

NZC is another guide with their stage 1 & 2.

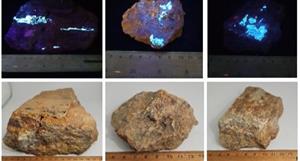

I recon LG Chem have a fair idea of what they are doing.. If they are onboard COB with concentrates with a dramatically lower grade than CLA, I think were looking fine from a met work perspective.

The only concerns about this project and the reason the market cap isnt much higher is strip ratio IMO. Be interesting to see how they tackle a combination of open pit and underground mining in the SS. COB will have an advantage in strip ratio for sure but lower grades across the board.

They can either sell a concentrate onwards to someone who would...

Add to My Watchlist

What is My Watchlist?