In this edition of Moves and Moods, we look at the nascent recovery among large cap lithium stocks.

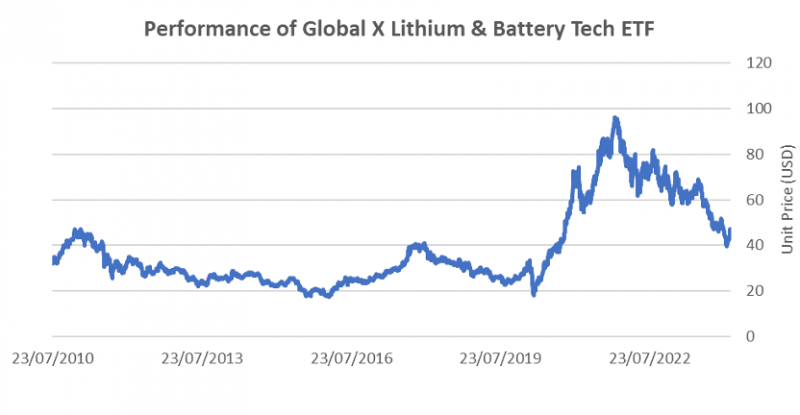

There are few indices that track the lithium market. However, the US listed LIT ETF from Global X does provide a history of over ten years, Figure 1. This index is broader than lithium miners and processors. It also includes battery makers such as Panasonic, LG Energy Solutions, Samsung SDI and Contemporary Amperex Technologies (CATL), as well as electric vehicle manufacturers Tesla and BYD.

Nonetheless, the picture reflects much of what has happened to stock prices over the past two years.

1. The Global X Lithium and Battery Tech ETF has experienced a drawdown of around 50% from the peak.

Clearly, the stock performance has been volatile.

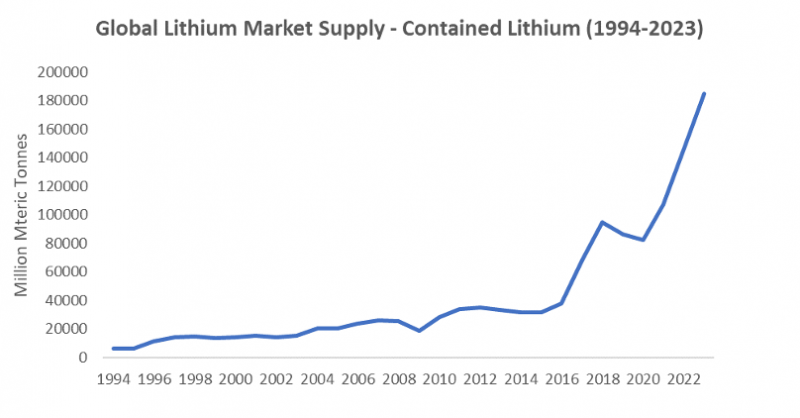

Global production data from the US Geological Survey (USGS), shows the sharp uptick in demand growth since the 2016 introduction of battery gigafactories by pioneering EV maker Tesla, Figure 2.

Forecasting new mine supply is clearly difficult.

2 The global production of lithium has trended up sharply since the advent of electric vehicles. Source: USGS.

Investment Opportunity

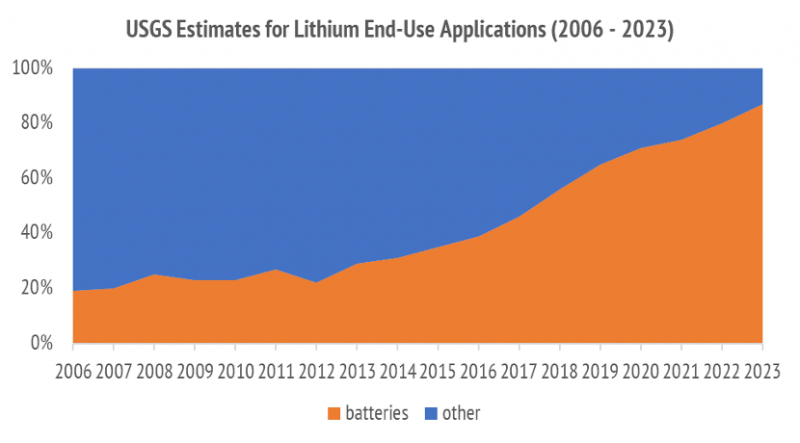

Evidently, the growth in the global lithium market has exploded since electric vehicles began to appear in ever larger volumes. Lithium-ion batteries are now the dominant use for lithium, Figure 3

3 Lithium-ion batteries gained market share rapidly in end-uses for lithium over the last decade. Source: USGS.

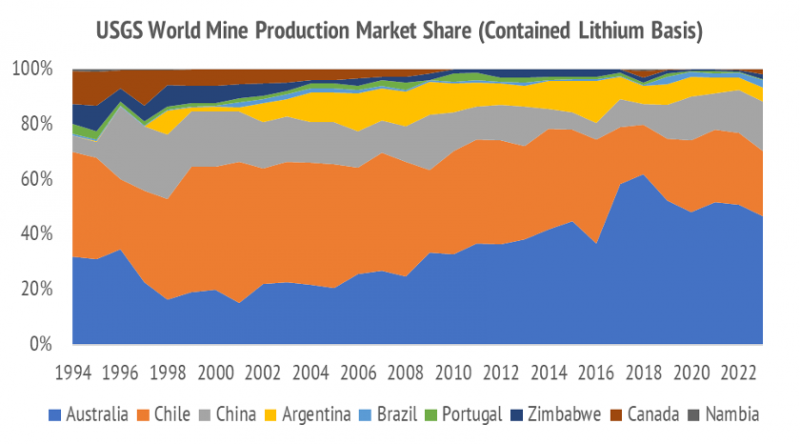

The advantage for Australian mineral producers is that hard rock spodumene sources of lithium can be brought into production more rapidly than other sources, such as salt-lake brines.

Australia remains the dominant source of lithium globally, with a current market share of 46.6 per cent, Figure 4.

4 Australia grew share of global lithium mining due to the relative ease of hard-rock mining. Source: USGS.

While the above market position is strong, the lithium battery industry requires more than just a simple concentrate. High purity lithium compounds such as lithium carbonate, lithium hydroxide, and lithium iron phosphate, are essential intermediates for the manufacture of lithium-ion batteries.

Since these involve capital and know-how intensive conversion plants, the industry structure is concentrated.

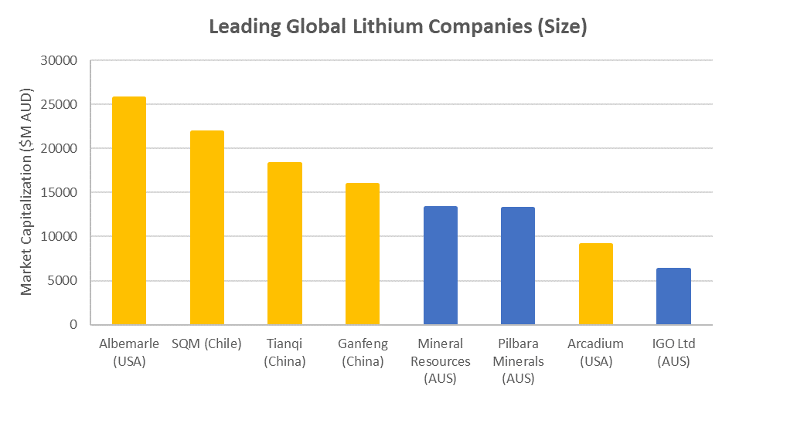

Globally, the lithium market is dominated by five vertically integrated mining and lithium conversion operations, Figure 5 (below).

For historical reasons, Albemarle (NYSE: ALB), SQM from Chile (NYSE: SQM), and the newly formed US conglomerate Arcadium Lithium (ASX: LTM) have dominated the ex-China market for lithium production and refining. This began to change with the rapid growth of the Chinese market and the chemical process innovations that occurred there. This began with conversion processes to upgrade spodumene concentrate to either lithium hydroxide or lithium carbonate. It has sped up in recent years with Chinese processing of hard rock lepidolite ores, and high magnesium ratio brines.

5 The big five vertically integrated lithium mining and conversion companies are show in in orange.

While we tend to think of China as a follower of Western innovations, this is no longer true in many areas of minerals processing and chemical engineering.

The combination of Chinese domestic demand, and innovations to drive faster plant construction and rollout, catapulted companies like Tianqi Lithium (HKG: 9696) and Ganfeng Lithium (HKG: 1772) to reach a similar scale to their offshore counterparts.

Increased demand in China drove a rapid expansion of Australian mining operations.

There are now three Australian miners with market capitalisation approaching the top four, Figure 5.

The largest pure play in Australia is Pilbara Minerals (ASX: PLS). Mineral Resources (ASX: MIN) is diversified into iron ore, mining services, energy, and lithium. IGO Ltd (ASX:IGO) is also diversified, with a 24.99 per cent holding of the famous Greenbushes mine, through a 49 per cent interest in a joint venture (JV) with Tianqi, that owns 51 per cent of that mine.

The other 49 per cent of Greenbushes is owned by Albemarle. Mineral Resources has two major lithium mines, Wodgina and Mt Marion, and owns a 50 per cent share in each. The other 50 per cent of Wodgina is owned by Albemarle, and the other 50 per cent of Mt Marion is owned by Ganfeng.

This partnering up of competitors is becoming more common due to the importance of process engineering know-how and offtake arrangements.

Move for This Mood

In some ways, the lithium market is becoming like the global petrochemical industry. Each player must carve out their own market share, but the projects are often difficult to bring into production at the necessary consistency and quality of product. This is due to the demanding specifications of battery makers downstream, and the difficulties caused by unwanted impurities in the midstream.

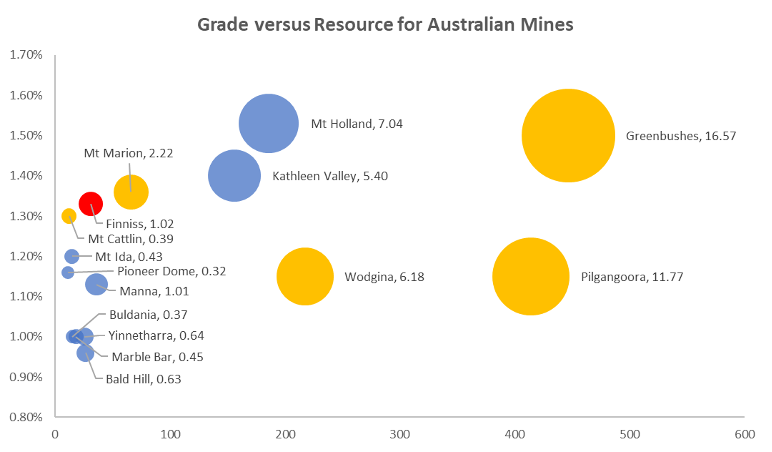

While there has been much excitement among explorers, the concentrated nature of the midstream and downstream market is creating its own power dynamics. Among the fifteen large Australian mine resources that are currently producing, or under development, there are just five giants, Figure 6.

6 The largest Australian resources are in the hands of major producers (orange) and developers (blue).

Mt Holland is 50 per cent owned by Wesfarmers and 50 per cent by SQM.

Greenbushes is 49 per cent owned by Albemarle and the remaining 51 per cent by the Tianqi JV, with a net 24.99 per cent falling to IGO Ltd. Wodgina and Mt Marion are 50 per cent owned by Mineral Resources, as described earlier.

This leaves just two large pure plays. The PIlgangoora Lithium Operation is 100 per cent owned by Pilbara Minerals, while Kathleen Valley is 100% per cent owned by Liontown Resources (ASX:LTR). There are promising new large prospective resources, such as the Andover Project developed by Azure Minerals (ASX:AZS). The same pattern is evident in the takeover offer now proceeding with backing from SQM and Gina Rinehart.

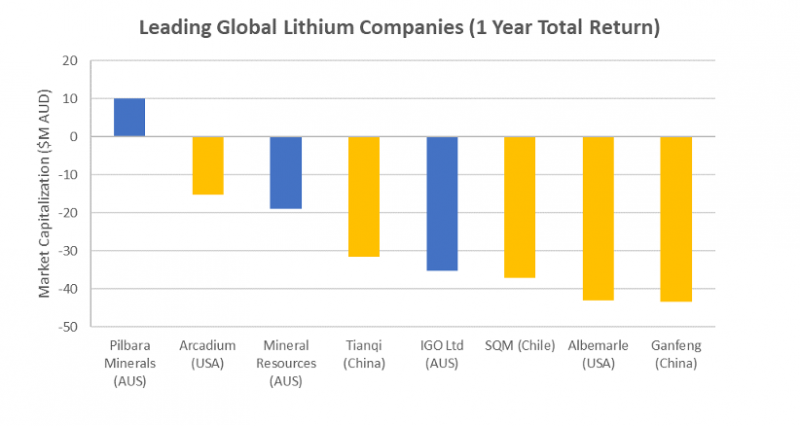

7 Only Pilbara Minerals has had a positive total return over the past year.

The stock performance has been grim, but Pilbara Minerals posted a positive one-year gain, Figure 7. The other players are all well positioned, and merger interest may return once lithium prices stabilize.

Disclosure: the author holds shares in Pilbara Minerals, IGO Ltd and SQM.

Disclaimer:This article contains information and educational content provided byJevons Global Pty Ltd, a Corporate Authorised Representative (AR1250727) of BR Securities Australia Pty Ltd (ABN 92 168 734 530) which holds an Australian Financial Services License (AFSL 456663). The Market Herald does not operate under a financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given.

The information is intended to be general in nature and is not personal financial advice. It does not take into account your personal financial situation or objectives and you should consider consulting a qualified financial professional before making any investment decision. All brands and trademarks included in this report remain the property of their owners.

The material provided in this article is for information only and should not be treated as investment advice. Viewers are encouraged to conduct their own research and consult with a certified financial advisor before making any investment decisions. For full disclaimer information, please click here.