In this edition of Moves and Moods, we follow up on the confirmed bull market in copper, gold, and uranium.

To this group we add the market action in silver, which typically follows major moves in gold. The positive moves in these commodities are supported by strength in oil.

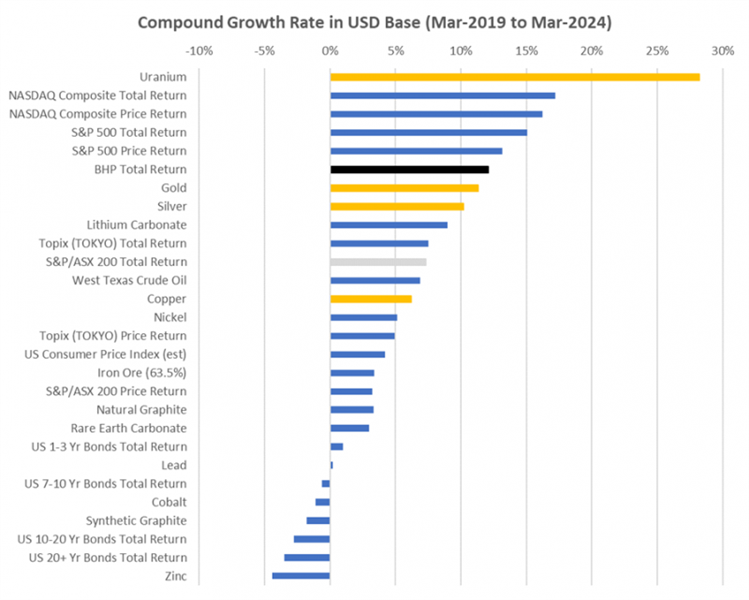

To put the recent moves in context, it is helpful to look back over the last five years (Figure 1).

1. Selected commodities, stocks, bonds, and US CPI Five Year Compound Annual Growth Rate (CAGR) Source: LSEG.

This chart reflects the annual rate of price change for commodities, along with the price return and total returns for major US stock indices, US bond indices, and the Australian and Japanese markets.

The numbers are all in US dollars, since the major source of credit creation worldwide remains the USA through the way in which the US Federal Reserve controls interest rates. The US dollar is also the main currency of international trade, in which our target commodities are priced.

Note that the US consumer price index is also included. This rose by 4.19% per annum over the last five years, with the last print being mid-February. I’ve estimated the number from that base over the corresponding five-year period. This small difference of timing is not that important.

Notice that inflation is supposed to have been licked, so markets are forecasting lower interest rates. Older investors, like me, who lived through the 1970s are not so sure. Gold just set a new all-time high above US$2,300. Of course, older folks, Chinese and Indians buy gold. Perhaps they agree with me?

Here I focus on BHP Group (ASX:BHP) – the one-stop shop for copper, gold, silver, and uranium exposure.

Investment Opportunity – stepping back to the 70s

ABBA fans across Australia know that the 1970s were not only about nervous shuffles to the strains of Dancing Queen, across the linoleum floor at the local Blue-Light Disco. Oil had only recently begun to rise, and so synthetic fabrics, like polyester, were very popular. So was central heating using fuel oil.

The Valiant Charger was a ride of choice for those who would not be seen dead in a Honda Civic.

Everybody knew that products made in Taiwan were cheap. Nobody knew if you should buy a Japanese car. Could they ever be the same quality as a US-made car, or even a Holden from Broadmeadows?

Slowly at first, and then all at once, this relaxed and comfortable worldview collapsed in a heap.

The Arabs in the Middle East decided to blockade the USA from buying oil to punish Israel for a war.

Oil prices soared, and so did inflation and interest rates. Stocks suffered a bad bear market.

The 1973-1974 bear market was bad in the USA. The Dow Jones index fell 45%.

Australia fared worse with the All Ordinaries Index down 59%.

This is all ancient history. It would not matter except for the fact that history is now rhyming so hard.

Australia had a fixed exchange rate and an economy that was protected by tariffs. This kept imports out, but it also juiced inflation.

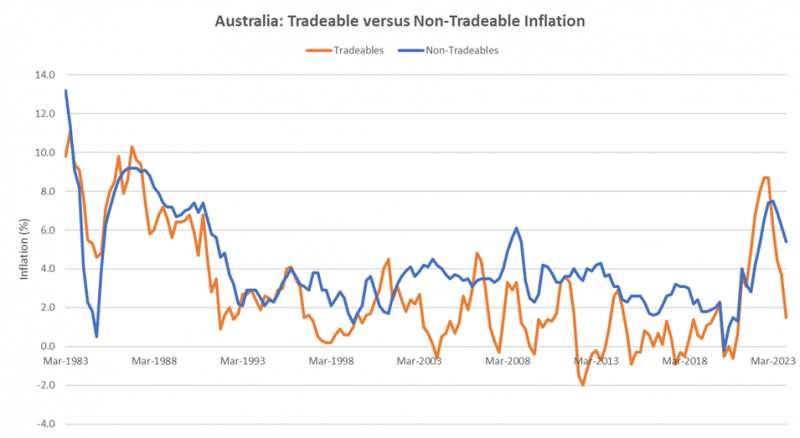

Only much later did Australia float the currency and begin the painful work of demolishing trade barriers. This shows up clearly in the different history of tradeable versus non-tradeable inflation measures, Figure 2.

The non-tradeable items include wages for local jobs and immobile factors like land prices. The tradeables are all the items that might be substituted via imports.

2 The problem for the Australian economy is the stubborn level of non-tradeables inflation. Source: ABS and RBA.

Notice that from the early 1990s the inflation for tradeables was much lower than non-tradeables. One big factor was the surge of manufactured goods from China. This had the effect of lowering inflation. This good deflation enabled a lower interest rate. This set off a housing boom.

The non-tradeables are now coming down, but only slowly.

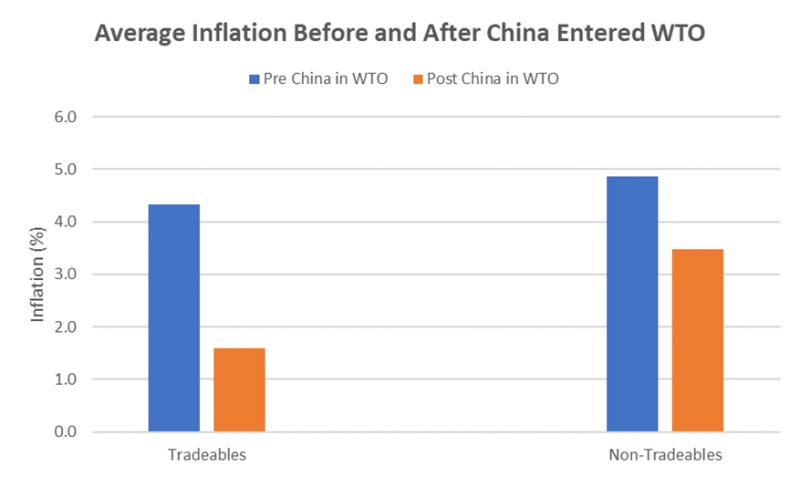

China entered the World Trade Organization (WTO) in December, 2001. This lowered inflation for traded goods, and widened the spread between tradeables and non-tradeables, Figure 3.

3 The effect of traded goods from China was clear in the data after they entered the WTO. Source: RBA and ABS.

The investment opportunity is a reversal of the previous global disinflation shock. The geopolitical pressures of the time have famously elevated national security concerns over the economy. Policies to reshore manufacturing, or friend-shore into more expensive locations, will raise goods prices.

Current policy initiatives are taking us straight back to the 1970s.

In the US, tariff walls are going up. In Australia, wages are going up. In Europe, energy is expensive.

Politicians are pushing policies that are indistinguishable from the failed adventures of my youth.

This will be a tough period in global markets and few folks under sixty have seen such conditions.

Gold and other safe-haven commodities, the must-have scarce items, are repricing upwards.

Move for this Mood

Oddly enough, Australia has one company that is very well positioned for these conditions.

BHP Group is the only company in the world that is a top-10 global copper miner as well as a top-10 global uranium producer. The source of the uranium, and a good chunk of the copper, as well as gold and silver by-products is the Olympic Dam mine in South Australia.

The market seems to have forgotten that 30% of BHP Group revenues come from copper. They have 57.5% ownership of the huge Escondida copper-porphyry mine in Chile, plus 100% of Olympic Dam, Prominent Hill and the recently acquired Carapateena operation in South Australia.

Uranium has not been a popular story among the ESG-focused institutions. They seem to have forgotten that Olympic Dam is the largest known uranium deposit on earth. The reserves are around 261,000 times, or one hundred times current production, in a resource of 2.1M tonnes. The grade is low at 0.05%, but the orebody is polymetallic. The revenue split includes copper (70%), uranium (25%), gold and silver (5%).

Historically, the big obstacle to mine expansion has been the availability of water. The Northern Water Supply Project (NWSP), in partnership with the South Australian government, may well solve this.

The energy transition needs copper for electrification and uranium for low-carbon nuclear fuel.

BHP Group, via Olympic Dam, is your one-stop shop for copper, gold, silver, and uranium.

Government spending on big infrastructure projects looks set to rise.

Profit from that to offset the likely lift in inflation.

Disclosure:The author holds shares in BHP Group.

Disclaimer:This article contains information and educational content provided byJevons Global Pty Ltd, a Corporate Authorised Representative (AR1250727) of BR Securities Australia Pty Ltd (ABN 92 168 734 530) which holds an Australian Financial Services License (AFSL 456663). The Market Herald does not operate under a financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given.

The information is intended to be general in nature and is not personal financial advice. It does not take into account your personal financial situation or objectives and you should consider consulting a qualified financial professional before making any investment decision. All brands and trademarks included in this report remain the property of their owners.

The material provided in this article is for information only and should not be treated as investment advice. Viewers are encouraged to conduct their own research and consult with a certified financial advisor before making any investment decisions. For full disclaimer information, please click here.